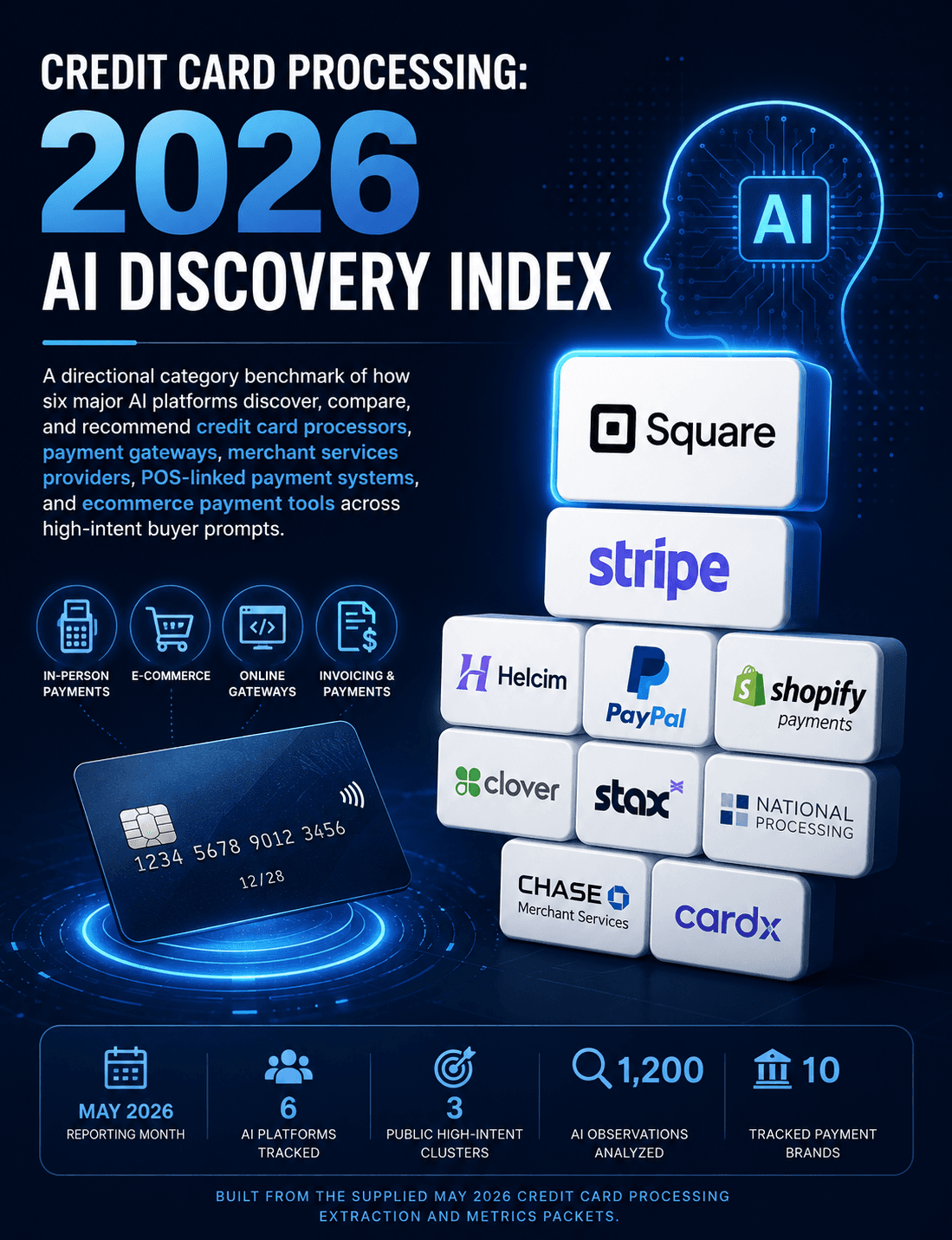

Credit Card Processing: 2026 AI Discovery Index

A directional category benchmark of how six major AI platforms discover, compare, and recommend credit card processors, payment gateways, merchant services providers, POS-linked payment systems, and ecommerce payment tools across high-intent buyer prompts.

May 2026

Reporting month

6

AI platforms tracked

3

Public high-intent clusters

1,200

AI observations analyzed

10

Tracked payment brands

On this page

- 01Answer Capsule

- 02Executive Summary

- 03The AI Discovery Shift in Credit Card Processing

- 04Directional Category Leaders

- 05The Buying Moments That Now Decide the Category

- 06Why Recommendation Power Is Concentrating

- 07The Category’s Most Visible Warning Sign

- 08What This Means for the Category

- 09What This Public Benchmark Does Not Include

- 10Methodology and Disclaimers

- 11CTA

Answer Capsule

In the May 2026 Credit Card Processing snapshot, AI recommendation power concentrates around Square and Stripe. Square is the clearest overall shortlist leader for small-business and POS-oriented payment acceptance. Stripe is the strongest online, developer, SaaS, and gateway-oriented challenger. Helcim, PayPal, Shopify Payments, Clover, and Stax each occupy useful specialist lanes, while CardX, National Processing, and Chase Merchant Services show materially weaker public shortlist capture.

Executive Summary

AI discovery in credit card processing is not behaving like a conventional merchant-services search page.

When a business owner asks an AI system for the best credit card processor, best payment gateway, best merchant service, cheapest processing option, or best invoicing/payment setup, the answer is usually not a neutral directory. It is a compressed shortlist.

That shortlist has a clear center of gravity.

Square is the strongest public benchmark leader. Across the full 1,200-observation snapshot, Square appears in 46.1% of observations, earns valid recommendation coverage in 41.7%, captures a 34.6% Top 3 recommendation rate, and holds a 20.8% rank-one recommendation rate. Its average recommended rank of 1.57 is the strongest among the tracked payment brands, and its modeled monthly captured recommendation value is the highest in the packet.

Stripe is the second major pole of the market. It appears in 35.8% of observations, earns valid recommendation coverage in 29.3%, captures a 24.8% Top 3 recommendation rate, and holds an 11.9% rank-one recommendation rate. Stripe’s average recommended rank of 1.69 signals that when it is recommended, it is often treated as a top-tier option rather than a backup processor.

The rest of the market is more use-case dependent. Helcim shows strong specialist authority around lower fees and transparent pricing. PayPal remains highly visible and commercially meaningful, but it is rarely the first answer. Shopify Payments and Clover win more naturally when the prompt includes ecommerce platform fit, retail, POS, or existing ecosystem context. Stax appears in high-volume or subscription-pricing contexts but does not approach Square or Stripe’s overall rank strength.

The public story is straightforward:

AI systems are turning payment processing from a vendor list into a use-case map.

Square owns “most small businesses.” Stripe owns “online, SaaS, and customizable gateways.” Helcim owns “lower fees and transparent pricing.” PayPal owns “quick setup and familiar checkout.” The brands without a sharply reinforced use case are less likely to be advanced into the shortlist.

The AI Discovery Shift in Credit Card Processing

Traditional SEO visibility in this category rewards ranking for terms like “best credit card processor,” “merchant services,” “payment gateway,” and “small business payment processing.”

AI discovery rewards something narrower: recommendation eligibility for a specific business type.

A restaurant, Shopify merchant, SaaS founder, contractor, retail store, nonprofit, high-risk merchant, and service business may all ask similar questions. But AI systems often route them into different provider lanes.

That routing changes the competitive field.

In a search results page, multiple processors can coexist as blue links. In an AI answer, the model often assigns roles: Square for in-person and small-business POS, Stripe for online and developer-led payments, PayPal for easy setup and invoicing, Helcim for transparent interchange-plus pricing, Shopify Payments for Shopify stores, Clover for retail and restaurant POS, Stax for high-volume subscription pricing, and National Processing for more specialized merchant-account contexts.

That means a brand can be present and still lose.

A processor might be mentioned as an integration, cited as a source, included in a comparison table, or referenced as an alternative. None of those outcomes carries the same commercial weight as being selected as one of the recommended processors.

The strongest category signal is not who is visible.

It is who gets advanced into the shortlist.

Directional Category Leaders

Brand | Directional AI role | Public benchmark signal |

Square | Overall small-business and POS leader | Highest valid recommendation coverage, Top 3 rate, rank-one capture, and modeled recommendation value |

Stripe | Online, SaaS, developer, and gateway leader | Second-strongest overall recommendation position and strong rank quality |

Helcim | Lower-fee and transparent-pricing specialist | Strong sentiment and meaningful Top 3 capture despite lower total modeled value |

PayPal | Familiar quick-setup and invoicing option | High visibility and modeled value, but weak first-position capture |

Shopify Payments | Shopify ecosystem specialist | Relevant when prompts are ecommerce-platform-specific |

Clover | Retail, restaurant, and POS specialist | Useful POS lane, weaker rank-one capture than Square |

Stax | High-volume and subscription-pricing specialist | Positive specialist framing, lower overall shortlist power |

National Processing | High-risk or merchant-account specialist | Narrow visibility and limited top-rank capture |

Chase Merchant Services | Bank-backed processing option | Some positive recommendation coverage, but no observed Top 3 capture in the public metrics |

CardX | Underexposed surcharge/compliance specialist | No measurable public recommendation capture in the supplied benchmark |

Square’s lead is not only a visibility lead. It is a rank-quality lead. Its 500 valid recommendations, 415 Top 3 recommendations, and 250 rank-one recommendations make it the most consistently selected tracked provider in the public snapshot.

Stripe’s second-place position is also structurally strong. It has fewer total appearances than Square, but when it is recommended, its average rank remains high. That suggests a clear role in AI-generated answers: Stripe is not a generic payment processor in these outputs. It is a specialist answer for online, technical, customizable, ecommerce, and subscription-oriented businesses.

Helcim is the clearest “smaller but trusted” specialist in the tracked set. It appears in 28.7% of observations and earns valid recommendation coverage in 26.8%, with no negative mentions in the supplied overall metrics and a strong net sentiment score. Its modeled value is lower than PayPal’s, but its recommendation framing is cleaner.

The Buying Moments That Now Decide the Category

The most important buying moment is still the broad “best processor” prompt.

Prompts such as “best merchant service for a small business,” “best credit card processing companies,” and “best payment gateways” are where AI systems form the first shortlist. In observed examples, those shortlists often place Square, Stripe, PayPal, Helcim, and Shopify Payments into distinct roles rather than treating them as interchangeable processors.

The second major buying moment is business-type fit.

Square benefits when the answer is organized around small business, retail, services, POS, and in-person payments. Stripe benefits when the answer is organized around online business, SaaS, subscriptions, ecommerce, customization, or developer control. Shopify Payments benefits when the buyer is already inside the Shopify ecosystem. Clover benefits when retail or restaurant hardware and POS workflow matter.

The third buying moment is pricing and fee evaluation.

This is where Helcim and Stax become more competitive. AI systems repeatedly need a clean way to explain interchange-plus pricing, subscription pricing, flat-rate pricing, monthly fees, hardware costs, chargebacks, and whether a processor is better for low-volume or high-volume merchants. In this lane, Square and Stripe still appear, but the “best overall” narrative can weaken if the user’s prompt emphasizes processing cost rather than convenience.

The fourth buying moment is trust and risk fit.

High-risk merchant accounts, chargebacks, frozen funds, underwriting, surcharging, and payment holds can reroute the answer away from the mass-market providers. In one observed high-risk merchant-account answer, National Processing was the only tracked brand included as a valid ranked recommendation, while Stripe and PayPal were referenced cautionarily in the context of merchants that may be shut down or denied.

The fifth buying moment is workflow adjacency.

Some prompts are not directly about merchant services. They are about invoicing, scheduling, ecommerce software, POS systems, or business software. In those answers, Stripe, Square, and PayPal may appear only as payment integrations rather than as the recommended product. That distinction matters. Integration visibility is not the same as processor recommendation.

Why Recommendation Power Is Concentrating

AI recommendation power in credit card processing appears to be shaped by a dense third-party evidence layer.

The extraction packet includes repeated citation examples from editorial, review, forum, and official-source environments, including NerdWallet, Forbes, Expert Market, Zapier, Reddit, Nav, Wise, credit-card-processing directories, processor blogs, and official payment or business-software pages. These sources do not merely supply facts. They help AI systems decide which provider belongs in which use case.

That evidence layer favors brands with simple, repeatable roles.

Square is easy to summarize: best overall for many small businesses, strong for POS, retail, services, and in-person payments.

Stripe is easy to summarize: best for online businesses, developers, SaaS, subscriptions, customization, and APIs.

Helcim is easy to summarize: lower fees, transparent pricing, and interchange-plus positioning.

PayPal is easy to summarize: quick setup, invoicing, brand familiarity, and broad consumer recognition.

Shopify Payments is easy to summarize: best if the business already runs on Shopify.

This is why recommendation power concentrates. AI systems appear to reward providers whose category role is reinforced across many third-party explanations.

The brands with less consistent framing are more exposed. A bank-backed merchant services provider, surcharge-compliance specialist, high-risk merchant account provider, or subscription-pricing processor may be highly relevant in the right scenario. But if the broad evidence layer does not repeatedly map that brand to a mainstream buyer problem, it may not enter the shortlist.

The Category’s Most Visible Warning Sign

The most visible warning sign is PayPal’s visibility-versus-first-choice gap.

PayPal is not weak in the public snapshot. It appears in 28.8% of observations, earns valid recommendation coverage in 20.3%, captures a 12.3% Top 3 recommendation rate, and has the second-highest modeled captured recommendation value among the non-Square/Stripe group. But its rank-one recommendation rate is only 0.33%, and its average recommended rank is 2.43.

That is a commercially important pattern.

AI systems clearly know PayPal. They include it often. They frame it positively in quick-setup, invoicing, and familiar-checkout contexts. But they rarely treat it as the best answer.

In traditional visibility reporting, PayPal could look healthy because it appears frequently.

In AI recommendation reporting, the story is different:

PayPal is present in the consideration set, but it is not controlling the decision slot.

A second warning sign sits at the specialist end of the market. CardX shows no measurable public recommendation capture in the supplied benchmark, and National Processing captures only minimal Top 3 share despite being relevant to a specialized merchant-account lane.

This does not prove those companies lack market value. It shows that broad AI discovery may not understand or surface their specialty unless the prompt explicitly activates it.

That is the specialist-brand problem in AI search:

The narrower the use case, the more important it is for the evidence layer to teach the model exactly when the brand should be recommended.

What This Means for the Category

Credit card processing brands are no longer competing only on rates, integrations, hardware, payment methods, and sales teams.

They are competing on machine-readable positioning.

The brands winning the public benchmark have clear AI-native roles:

Square is the default small-business answer.

Stripe is the default online and technical answer.

Helcim is the transparent-pricing answer.

PayPal is the quick-start and familiar-checkout answer.

Shopify Payments is the Shopify-native answer.

Clover is the POS-system answer.

That role clarity matters because AI systems compress merchant evaluation into a few buyer-fit categories. A provider that cannot be summarized cleanly may still be visible, but it will be harder to recommend.

This creates two strategic pressures for the category.

First, broad processors need to defend their generic “best” prompts. These are the prompts where Square and Stripe are currently strongest and where future challengers must prove they deserve shortlist placement.

Second, specialist processors need to own their exact trigger moments. High-risk merchants, surcharge programs, high-volume processing, B2B payments, nonprofits, restaurants, healthcare, field services, multi-location retailers, and ecommerce platforms each represent separate AI routing paths.

The next competitive frontier is not just content volume.

It is recommendation architecture: the repeated external proof that tells AI systems when a provider is the right answer.

What This Public Benchmark Does Not Include

This public version intentionally shows only the category shape.

It does not include the full competitor threat profiles, platform-by-platform loss map, prompt-by-prompt diagnosis, citation failure map, source remediation plan, or full recovery roadmap.

It also does not include raw prompt dumps or the full scoring logic behind recommendation validity and modeled value.

Those layers are withheld because they explain exactly why a specific payment brand is being displaced and what must change to recover AI recommendation power.

The public conclusion is directional:

Square and Stripe currently control the strongest AI shortlist positions in the observed credit card processing prompt universe. Helcim, PayPal, Shopify Payments, Clover, and Stax hold meaningful use-case lanes. Specialist and bank-backed providers appear much more dependent on prompt specificity.

Methodology and Disclaimers

This benchmark is based on the supplied May 2026 Credit Card Processing extraction and metrics packets. The tracked company universe includes Stripe, CardX, Chase Merchant Services, Clover, Helcim, National Processing, PayPal, Shopify Payments, Square, and Stax. The public metrics packet reports 1,200 observations and platform coverage across ChatGPT, Gemini, Microsoft Copilot, Perplexity, Google AI Mode, and Google AI Overviews.

The analysis separates presence from valid recommendation coverage. Presence means a brand appeared in an AI answer. Valid recommendation coverage means the brand was advanced as a recommendation-level option, not merely mentioned as an integration, cited as a source, or referenced in passing.

The public scope includes three high-intent cluster types: best/top payment processors and gateways, comparison or head-to-head evaluation, and pricing or cost evaluation. The supplied aggregation is heavily weighted toward best-of and gateway discovery prompts, with much thinner usable coverage in comparison and pricing clusters. Some internal cluster labels appear inherited from a prior template; this public report names clusters by observed credit card processing prompt intent rather than by those template labels.

Modeled monthly captured recommendation value is not booked revenue. It is a directional benchmark used to compare the relative commercial weight of recommendation capture across tracked prompts.

This report does not evaluate processor pricing accuracy, underwriting quality, contract terms, fraud risk, chargeback policies, regulatory compliance, or merchant suitability. It evaluates AI discovery behavior and recommendation patterns.

CTA

For payment processors, merchant services providers, POS platforms, payment gateways, and fintech marketing teams, the full LLM Authority Index deep-dive identifies the exact prompts, platforms, citation sources, competitor framings, and evidence gaps behind lost AI recommendation power. The public benchmark shows the category pattern. The paid diagnostic shows where a specific brand is losing and what has to change.

Want the full Authority Index for Credit Card Processing?

The paid deep-dive adds competitor threat profiles, the gap matrix, citation failure map, platform-by-platform recovery roadmap, and client-specific economic modeling.