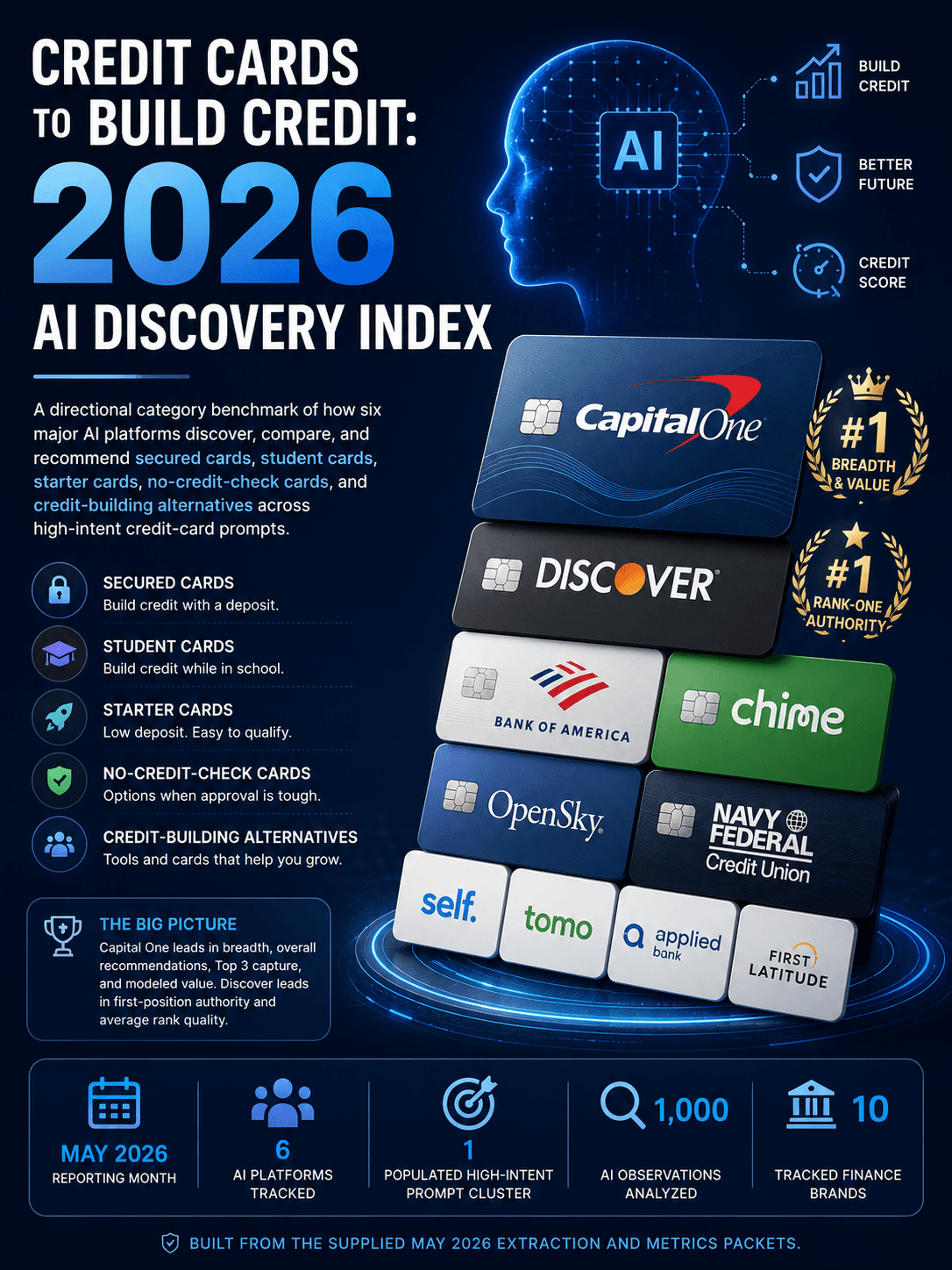

Credit Cards to Build Credit: 2026 AI Discovery Index

A directional category benchmark of how six major AI platforms discover, compare, and recommend secured cards, student cards, starter cards, no-credit-check cards, and credit-building alternatives across high-intent credit-card prompts.

May 2026

Reporting month

6

AI platforms tracked

1

Populated high-intent prompt cluster

1,000

AI observations analyzed

10

Tracked finance brands

On this page

- 01Answer Capsule

- 02Executive Summary

- 03The AI Discovery Shift in Credit Cards to Build Credit

- 04Directional Category Leaders

- 05The Buying Moments That Now Decide the Category

- 06Why Recommendation Power Is Concentrating

- 07The Category’s Most Visible Warning Sign

- 08What This Means for the Category

- 09What This Public Benchmark Does Not Include

- 10Methodology and Disclaimers

- 11CTA

Answer Capsule

In the May 2026 “credit cards to build credit” snapshot, AI recommendation power concentrates around Capital One and Discover. Capital One leads breadth, overall recommendation coverage, Top 3 capture, and modeled recommendation value. Discover has the strongest first-position signal and the best average recommended rank. Bank of America is the main mainstream-bank challenger, while Chime and OpenSky win narrower no-credit-check and credit-repair-style moments.

Executive Summary

AI discovery in credit cards for building credit is not forming around one simple “best card.”

It is forming around borrower situations.

When users ask which card is best to build credit, AI systems usually route the answer into a few repeatable lanes: best overall secured card, low-deposit starter card, student card, no-credit-check card, cash-back secured card, high-credit-limit secured card, and credit-union or member-specific option.

That routing determines who gets recommended.

Across the full 1,000-observation public snapshot, Capital One is the broadest AI recommendation leader. It appears in 70.2% of observations, earns valid recommendation coverage in 65.5%, captures a 52.6% Top 3 recommendation rate, and holds the highest modeled monthly captured recommendation value in the tracked set.

Discover is the strongest rank-quality challenger. It appears in 60.1% of observations and earns valid recommendation coverage in 54.5%, but its standout signal is first-position capture: Discover has a 26.0% rank-one recommendation rate, higher than Capital One’s 15.0%. Its average recommended rank of 1.53 is also stronger than Capital One’s 1.87.

That creates the category’s central public story:

Capital One wins breadth. Discover wins “best overall” authority.

Bank of America, Chime, OpenSky, and Navy Federal Credit Union form the next tier, but each wins in a more specific way. Bank of America appears as a mainstream secured or student-card option. Chime is strongest when the prompt emphasizes no credit check or an alternative credit-builder product. OpenSky appears more often in credit-repair and no-credit-check secured-card contexts. Navy Federal has lower overall coverage, but when it appears, it can rank strongly in the right credit-union or member-oriented moment.

The AI Discovery Shift in Credit Cards to Build Credit

Traditional search visibility in this category rewards pages about “best secured cards,” “best student credit cards,” “cards for no credit,” and “how to build credit.”

AI discovery rewards something more commercially decisive: assignment to the user’s next financial step.

A consumer does not simply ask for a credit card. They ask from a situation:

They may have no credit history.

They may be a student.

They may be rebuilding after damaged credit.

They may want a low deposit.

They may want cash back while building credit.

They may be worried about being denied.

They may want a card that reports to the bureaus.

AI systems compress those situations into shortlists. That means the winning brand is not always the one with the most pages, the most name recognition, or the broadest banking footprint. It is the brand that AI systems can confidently map to a borrower scenario.

This is why presence and recommendation coverage must be separated.

A brand can appear as a citation, a card example, a bank, a credit-builder tool, or a factual reference. That does not mean it was recommended. The strongest category signal is not who is visible.

It is who gets advanced into the shortlist.

Directional Category Leaders

Brand | Directional AI role | Public benchmark signal |

Capital One | Broadest starter-card and low-deposit leader | Highest valid recommendation coverage, Top 3 capture, raw presence, and modeled value |

Discover | “Best overall” secured-card authority | Highest rank-one rate and strongest average recommended rank among major leaders |

Bank of America | Mainstream-bank secured and student-card challenger | Third-highest valid recommendation coverage and strong modeled value |

Chime | No-credit-check and alternative credit-builder specialist | Strong positive framing, especially where prompts focus on approval friction |

OpenSky | Credit-repair and no-credit-check secured-card specialist | Narrower but clear specialist lane |

Navy Federal Credit Union | Member and credit-union option | Lower coverage, but meaningful modeled value and strong rank when eligible |

Self, Tomo, Applied Bank, First Latitude | Underexposed or niche tracked options | Very limited public shortlist capture in this snapshot |

Capital One’s lead is structural. It is not just mentioned more often. It is recommended more often. Its 655 valid recommendations, 526 Top 3 recommendations, and 150 rank-one recommendations make it the broadest public AI winner in the tracked set.

Discover’s position is different. It is not the broadest by total recommendation coverage, but it is the most frequently treated as the first answer. In the extraction examples, Discover is repeatedly framed as “best overall,” especially around secured-card and build-credit prompts.

Bank of America holds a meaningful third position, with 36.1% valid recommendation coverage and 16.9% Top 3 capture. That places it ahead of specialist alternatives in breadth, but behind Capital One and Discover in both recommendation scale and rank quality.

Chime and OpenSky show why specialist positioning matters. Chime’s overall valid recommendation coverage is 28.4%, while OpenSky’s is 15.9%. Neither controls the whole category, but both become more relevant when AI systems interpret the user as needing a no-credit-check, no-deposit, or credit-rebuilding path.

The Buying Moments That Now Decide the Category

The public snapshot is dominated by best-of and discovery-style credit-card prompts. The most commercially important prompts are not generic education prompts. They are prompts where a user is asking AI to choose a card.

The first buying moment is “best credit card to build credit.”

In this lane, AI answers often produce a shortlist rather than a tutorial. Observed outputs include Discover, Capital One, Chime, OpenSky, and Bank of America in different roles: Discover as best overall, Capital One as low-deposit or simple cash-back secured, Chime as no-credit-check, OpenSky as no-credit-check or credit-repair, and Bank of America as a mainstream secured-card option.

The second buying moment is secured-card selection.

This is where Discover’s rank quality is most visible. In observed secured-card prompts, Discover is repeatedly framed as best overall or best for rewards. Capital One appears as a low-deposit option, Bank of America as a high-credit-limit or secured-cash-rewards option, OpenSky as a no-credit-check or credit-repair option, and Chime as a no-credit-check alternative in some outputs.

The third buying moment is student credit cards.

Student-card prompts are commercially important because they catch consumers at the start of their credit lives. In one observed “best student credit cards” prompt, the valid recommendation list included Discover, Capital One, and Bank of America, with Capital One appearing through multiple student-card variants.

The fourth buying moment is approval anxiety.

Prompts like “best card to fix your credit,” “best card if I keep getting denied,” or “best no-credit-check card” shift the answer away from broad mainstream-bank logic. Chime and OpenSky become more eligible because they are easier for AI systems to explain as alternatives for consumers who may not qualify for traditional cards. In observed examples, Chime is framed as a no-credit-check credit-builder option, while OpenSky is framed as a credit-repair or no-credit-check secured-card option.

The fifth buying moment is credit-union or member-specific trust.

Navy Federal Credit Union does not have the same broad recommendation coverage as Capital One or Discover. But its average recommended rank and modeled value suggest that when the prompt or source environment makes a credit-union/member-specific option relevant, Navy Federal can be a meaningful competitor.

Why Recommendation Power Is Concentrating

Credit cards for building credit are a trust-heavy consumer finance category. AI systems appear to rely heavily on third-party card-comparison and financial education sources, plus official issuer pages when product specifics matter.

The observed source environment includes Bankrate, NerdWallet, WalletHub, Discover official pages, Bank of America official pages, Chime official pages, Capital One official pages, Experian, LendingTree, CardRatings, Forbes, Finance Yahoo, YouTube, and other review or editorial sources.

That source mix favors brands with clear, repeated category labels.

Discover benefits because the evidence layer repeatedly supports a simple story: best overall secured card, rewards while building credit, and beginner-friendly secured-card positioning.

Capital One benefits because its products map cleanly to multiple roles: low deposit, secured cash back, starter cards, student cards, and general build-credit use cases.

Bank of America benefits because it is a familiar mainstream bank with secured and student-card products that can be inserted into comparison-style answers.

Chime benefits when the question is less about traditional secured cards and more about approval friction.

OpenSky benefits when the prompt is closer to no-credit-check or credit-rebuilding anxiety.

This is not only about being cited.

A brand can be cited as a source and still fail to become a recommendation. In one observed example, a Navy Federal page appeared as a source label, but the brand was excluded from the recommendation layer because it was not presented as a company option in the answer.

That distinction is the category’s new competitive reality.

The AI answer may use a brand’s page to support someone else’s recommendation.

The Category’s Most Visible Warning Sign

The most visible warning sign is the gap between broad financial relevance and credit-card recommendation eligibility.

Self, Tomo, Applied Bank, and First Latitude are tracked in the category, but the public metrics show very limited shortlist capture. Self appears in 3.5% of observations and earns valid recommendation coverage in 2.9%. Tomo appears in 1.0% and earns recommendation coverage in 0.7%. Applied Bank and First Latitude each record only 0.1% recommendation coverage in the public snapshot.

That does not mean these brands have no consumer relevance.

It means AI systems are not often selecting them as the answer inside this observed build-credit card journey.

For challenger brands, this is the core risk:

A product can be designed for credit building and still be absent from the AI shortlist.

The issue is not simply awareness. It is machine-readable fit. AI systems need enough repeated third-party and official evidence to understand when a product should be recommended, for whom, and against which alternatives.

There is a second warning sign for larger incumbents: rank dilution.

Bank of America has meaningful visibility and recommendation coverage, but it does not match Discover’s first-position strength or Capital One’s breadth. Chime has strong sentiment and a clear use case, but its average recommended rank is weaker than the leaders. OpenSky is clearly recognized in specialist no-credit-check contexts, but its coverage is far below the two dominant brands.

In AI discovery, being in the answer is not enough.

Being third, fourth, or “also consider” can still mean losing the application moment.

What This Means for the Category

The market for credit cards that build credit is becoming more scenario-driven.

Brands need to win a role, not just a keyword.

Capital One currently owns the broadest role: starter-card flexibility across secured, student, low-deposit, and general build-credit prompts.

Discover owns the strongest “best overall” role: the card AI systems often name first when the prompt is about secured cards or building credit with a trusted beginner product.

Bank of America owns a credible mainstream-bank role, but it does not yet appear to control a category-defining position in the public benchmark.

Chime owns the alternative approval-friction role.

OpenSky owns the no-credit-check and credit-repair-style role.

Navy Federal owns a narrower credit-union/member trust role.

The implication is clear:

AI systems are not merely listing credit cards. They are assigning credit-building pathways.

That means the next competitive frontier is not just having a secured card, student card, or credit-builder product. It is making the product’s eligibility, use case, reporting behavior, approval path, costs, limits, and borrower fit consistently legible across the sources AI systems use to construct answers.

For issuers and fintechs, the commercial risk is that AI shortlists compress the category. A consumer may not review twenty cards. They may ask once, receive five names, and apply from there.

What This Public Benchmark Does Not Include

This public version intentionally shows only the shape of the market.

It does not include the full competitor threat profiles, the complete gap matrix, the exact citation failure map, the platform-by-platform remediation plan, or the prompt-level recovery roadmap.

It also does not show raw prompt dumps or the full scoring logic behind recommendation validity and modeled value.

Those layers are withheld because they explain exactly why a specific card issuer or fintech is being displaced and what must change to recover recommendation power.

The public conclusion is directional:

Capital One and Discover currently control the strongest AI recommendation positions in the observed “credit cards to build credit” prompt universe. Bank of America is the strongest mainstream-bank challenger. Chime and OpenSky have useful specialist lanes. Navy Federal Credit Union has narrower but meaningful rank/value potential. Self, Tomo, Applied Bank, and First Latitude appear underexposed in the public shortlist layer.

Methodology and Disclaimers

This benchmark is based on supplied May 2026 extraction and metrics aggregation packets covering 1,000 AI observations across ChatGPT, Gemini, Microsoft Copilot, Perplexity, Google AI Mode, and Google AI Overviews. The tracked company universe includes Navy Federal Credit Union, Applied Bank, Bank of America, Capital One, Chime, Discover, First Latitude, OpenSky, Self, and Tomo.

The analysis separates presence from valid recommendation coverage. Presence means a brand appeared in an AI answer. Valid recommendation coverage means the brand was advanced as a recommendation-level option, not merely mentioned, cited, or referenced as a source.

The supplied metrics packet contains three public cluster containers, but only one populated observation cluster in the aggregate. This report therefore treats the public read as a discovery and best-of benchmark for credit cards used to build or rebuild credit, rather than as a full comparison, pricing, or review census.

Some supplied cluster labels appear broad or inherited from another template. The report interprets the data by observed prompt intent: secured cards, student cards, starter cards, no-credit-check cards, and credit-building card recommendations.

Modeled monthly captured recommendation value is not booked revenue. It is a directional benchmark used to compare the relative commercial weight of recommendation capture across the tracked prompts.

This report does not provide financial advice, credit-card recommendations for individual consumers, underwriting guidance, APR validation, or suitability analysis. It evaluates AI discovery behavior and recommendation patterns.

CTA

For credit card issuers, fintechs, banks, credit unions, and credit-builder brands, the full LLM Authority Index deep-dive identifies the exact prompts, platforms, citations, competitor framings, and evidence gaps behind lost AI recommendation power. The public benchmark shows the category pattern. The paid diagnostic shows where a specific brand is losing and what has to change.

Want the full Authority Index for Credit Cards to Build Credit?

The paid deep-dive adds competitor threat profiles, the gap matrix, citation failure map, platform-by-platform recovery roadmap, and client-specific economic modeling.